Written by Gary Markham, Land Family Business

147% of the profit of the average arable farm is BPS

Farming is embarking on a period of change that most of the current generation of farmers have not experienced. Moving from the comfort of area payments to having to apply for specific funding for providing natural capital. This will inevitably put farming business in financial strain as there will be a funding gap between the two regimes over the forthcoming few years. The benchmarking of the Land Family Business (LFB) clients compared with the Groundswell Group over the past 4 years has produced some very interesting results.

1) There is a huge reliance on BPS for profitability

• 147% of profit in the average LFB group for the 2020 harvest consists of BPS

• In the previous 2019 harvest it was 84%

• 53% of the profit in the top 25% LFB group for both harvest consists of BPS

• Percentage reduction in BPS on average LFB clients is 22% in 2021

2) The amount of capital locked into the system relative to profitability is far greater than any other business

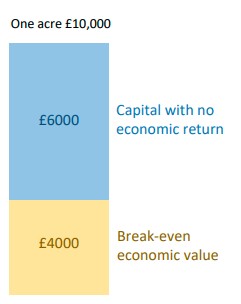

• The break-even economic value of arable land based on an average gross margin less fuel costs is in the region of £4,000 per acre.

• The additional £4,000 to £6,000 per acre up to market value has no bearing on the productive capacity. This additional capital tied up in a farming business does not contribute in any way – apart from occasionally some development sale

• The capital cost of machinery over the past few years has increased to over £300 per acre

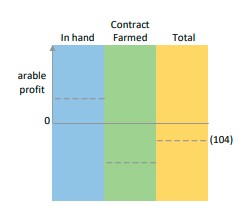

Many farmers have quite correctly attempted to expand in acreage as a means of dealing with these pressures. However, expanding acres has normally meant tendering for contract farming agreements. The benchmarking results have consistently shown over several years. An average a loss of between £40 to £60 per acre is made on the additional land.

Does this point to arable farming, producing commodity crops, perhaps not being a viable business model? The margin from arable farming before BPS and income from other enterprises, has been a loss of £2 per acre in the 2018 and 2019 harvests and has dropped to a loss of £104 per acre in the LFB benchmarking survey for the 2020 harvest. Change is inevitable – but managing the change is where the difficulty comes. One of the best tools to monitor the change and provide achievable targets is to benchmark against farming businesses that have already made or are making these changes.

Groundswell Benchmarking Group

LFB have been benchmarking a group of regenerative agriculture farming businesses for the 2017 to 2020 harvests – to identify if regenerative agricultural production systems can be financially viable.

Some of the key findings for the regenerative systems are

• the average output per acre is around 20% to 25% lower

• variable costs are around 20% lower

• gross margin 25% lower

• labour and machinery costs are around 30% lower

This results in a very similar average gross margin after labour and machinery for both systems of production. However, the range of results within the Group is wide with the top performers achieving results well above conventional top 25% group.

• LFB margin range (£102) to £47

• Groundswell margin range (£90) to £102

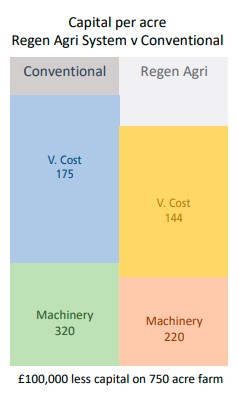

In addition to margins there are savings in working capital of around £135 per acre which can have a large impact on a farming business

• savings in machinery capital of around £100 per acre

• savings in variable costs of around £35 per acre

Total saving per acre £135 which on a 750 acre farm amounts to over £100,000

Machinery Capital per Tonne

The main influencers of profitability in arable farms are

• the machinery costs and in particular depreciation which represents the capital per acre

• yields

We have therefore developed a key indicator: machinery capital per tonne of winter wheat to compare regenerative agriculture with conventional methods

• Groundswell group average for 2020 harvest £95

• LFB conventional system £100

The difference has been around £20 to £30 per tonne over the past 4 harvests.

Cost of production per tonne

The total cost of production per tonne, widely used in the industry as a key performance indicator is a flawed concept as a management tool because of two factors:

• In production economics it is the marginal cost that is important – therefore the cost of production will vary with which tonne is being assessed – the law of diminishing returns applies here

• the ultimate test is the quantum of profit produced per acre. A very low cost per tonne on a low yield may deliver less total profit than a higher cost on a higher yield.

However, the 2020 harvest yields of wheat are

• 29% lower than 2019 harvest in the LFB Group

• 18% lower than 2019 harvest in the Groundswell Group

• Average cost per tonne in the LFB group is £130

• Average cost per tonne in the Groundswell Group is £98

So, what does all this mean?

Firstly, traditional ‘yield is king’ philosophy works at higher grain prices such as spring 2021 prices of approaching £200 per tonne. The marginal cost of production can be higher to continue a positive margin on the diminishing returns curve.

However, on average prices, a new approach is required and it seems that the regenerative agricultural system may be more robust in the medium to long term. Secondly, expanding acres is not feasible by using traditional contract farming structures; true joint ventures need to be used. Thirdly benchmarking data from four harvests proves that there is a different approach that is economically viable.

Joint Ventures

Many farming businesses would benefit from collaboration. There are economic benefits but equally important are the personal wellbeing benefits to the individuals. The benchmarking results show that competitively tendering for contract farming agreements does not work for all parties as they are not true joint ventures. A system that is tried and tested is the machinery syndicate together with a share farming agreement. In these arrangements the costs are shared and equally the output and margin are shared whilst robustly retaining the individual businesses in the eyes of HMRC.

These models are ideal for the transition from a traditional production system to a regenerative agriculture lower cost system.

• it will allow the investment in new machinery to be shared

• knowledge sharing amongst the group in a new system

• working within a group has a positive influence on general wellbeing

• will enable the farming businesses as a total, to take advantage of the forthcoming environmental land management schemes..